♣ CLICK THIS TO STOP TRYING TO ACHIEVE YOUR GOALS BY YOURSELF AND BE COACHED TODAY HERE

♥ CLICK THIS TO DOWNLOAD THIS FREE PDF SUMMARY HERE

♦ CLICK THESE FOR THE FOLLOWING Book | Summaries | Course

YouTube |Spotify | Instagram | Facebook | Newsletter | Website

Summary of Value Investing: From Graham To Buffett And Beyond

Advertisements

The book is comprehensive guidelines on stock evaluation and differences among methods used by generations of investors under the basic concept “Value investing”. Value investing is buying stock at a discount price below its intrinsic value. A gap between purchased price and intrinsic value is “Margin of safety” that helps to absorb risks and mistakes in the valuation process.

Some highlights separate value investors from speculators:

– Value investors operate in their circle of competencies. They tend to choose securities of companies that they can easily learn about and have a low (reasonable) price

– Most of value investors are micro fundamentalists. Their research on promising investments has a bottom-up approach – they start by looking at stock one by one.

Process of investing includes answering five important questions: What securities? -> Their intrinsic values? -> Margin of safety? -> Price to buy? -> When to sell? The book emphasizes the second question.

- SCREENING TECHNIQUES

When screening a potential investment, there are four types of variables investors can consider: Fundamental, technical, combined variables and market capitalization.

1/ Fundamental variables focus on economics of the business, not market opinions about it, e.g.: ROE/ROI, growth in EPS/sales/assets and profit margins. Historical data shows that firms with in low level of those ratios tend to provide higher returns in the future.

2/ Technical variables are totally opposite to fundamental ones when their concentrations are trend lines and market momentum. This is not what value investors pay much attention to.

3/ Combined ones mix the above two types of variables together, they are ratios such as P/E, P/CF, P/B, P/S and dividend yield. Again, firms having low results in those ratios seem to provide higher return than those with high variables.

4/ Market capitalization concerns sizes of companies and their likeliness to outperform. In general, small companies tend to offer more bargains than big firms do.

With the development of Internet and spread of value investing philosophy, it is not easy to spot a promising investment nowadays. However, as the author wrote, investors can consider some circumstances when opportunities are likely to emerge. Small or spin-off companies can give precious chances to invest because they are often obscure securities, probably missed by professional investors. That does not mean those companies are not good, just their financial statements are a bit confusing and/or ambiguous. Plus, the size of those firms is small has discouraged professional investors from rigorous research on those securities.

Under the same logic, investors can consider boring businesses that are making slow growth and modest profits. They are unlikely to attract much attention from the market, thus, any of their positive changes in operations, management, etc. are unnoticed.

In addition, investors can think of stock that is undesirable by the market, and thus, mispriced. Those are securities of businesses having financial distresses, overcapacity, and legislation punishment or lagging behind markets. Some problems lead to a dead-end but some only exist temporarily. Market’s lack of ability to estimate the impact of businesses’ trouble and its overreaction sometimes result a deep discount on stock price, which is an opportunity for value investors to purchase.

Of course, those opportunities need to go hand in hand with low/reasonable stock prices and profitable catalysts in order to benefit investors in the future.

- INTRINSIC VALUE

The authors did not include Discount Cash Flow (DCF) model and multiple-based method in their consideration despite the two are very popular in stock evaluation and are commonly taught at business schools. Because DCF, which requires the estimation of future cash flows in the next 10 years and beyond, seems to be risky if not impossible to implement without mistakes. No one can accurately predict what will happen in the business, industry and economy in next decades. Meanwhile, this method depends on the accuracy of variable; any small changes in value of underlying assumptions can cause a big change in calculated intrinsic value.

Multiple-based method, using combined variables as we mentioned above to estimate intrinsic value, also has several problems in it. Typically, investors tend to take earning, EBITDA or EBIT of their target companies multiplied by variable of comparable firms on stock market. In other word, they are pricing securities based on someone’s else uncertain projection for another company. Secondly, we all know that it is hard to find a 100% comparable companies to have enough confidence in the multiplication results. Finally, this method fails to employ fundamental economics of the companies like profit margin, competitive advantage, etc.

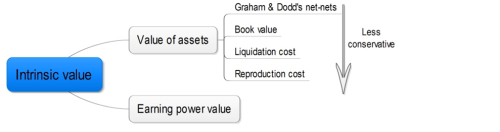

Two broad categories of methods mentioned in the book are Value of Assets and Earning Power Value (EPV):

2.1 Value of assets

Graham & Dodd’s net-nets

Intrinsic value = Current asset (book value) – liabilities (book value)

Comment: The underlying of this formula is that companies are in a non-viable or declining industry that they are going to sell assets and get out of business soon. The formula assumes that only current assets, which are liquid and marked to the market, are valuable when companies are going out of business. This way of calculating intrinsic value is simple. However, nowadays it is hard or even impossible to find stock at that low price because Graham’s idea has been out for decades and computers make any calculations become easy.

Book value

Intrinsic value = Total assets (book value) – Liabilities

Comment: The authors did not mention much about this method but they said its result of intrinsic value is hard to beat. It is still a conservative and simple way to estimate value but it is anyway more open than the net-nets.

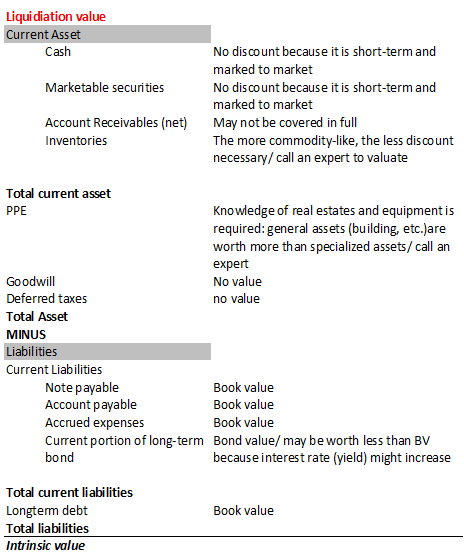

Liquidation cost and reproduction cost

Idea behind liquidation costs supposes that the company under consideration is operating in a declining industry which is the same in the above two methods. Nevertheless, this method gives some values to properties, plants, and equipment (PPE) while still assumes that intangibles and highly specialized assets have no value at all.

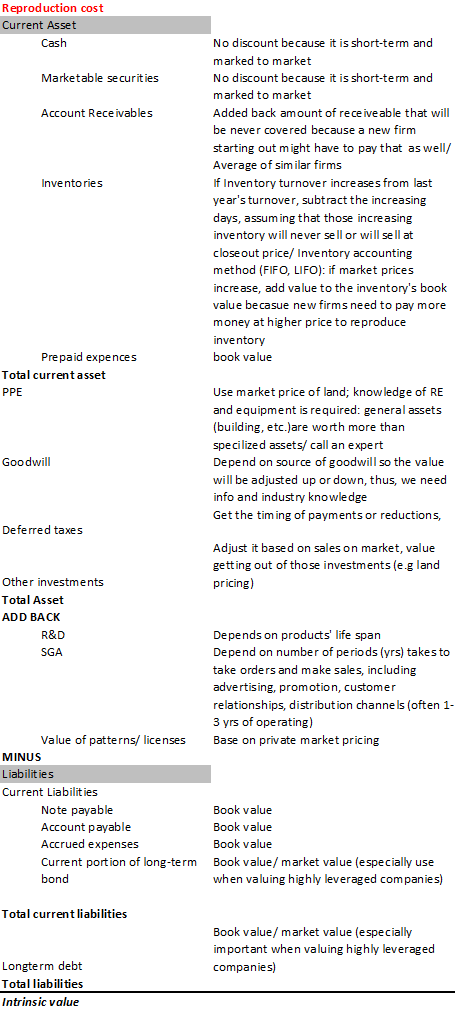

On the other hand, reproduction means company is in a viable, going industry so it will be last for a long time. However, this kind of industry is highly competitive and having no barrier to entry. Therefore, value of the company, or stock, will depend on how much a new comer has to spend in order to operate in the market. With this way of calculation, we give some values for intangibles because new comers must pay some time and money to build brands, R&D or customer relations in order to have a position in the industry.

Picture below illustrates how to apply liquidation and reproduction costs into estimating value of stock. “/” means “or”. For some items on the balance sheet, there is more than one way to estimate their values. Sometimes, it is helpful to ask for valuation from industry experts.

2.2 Earning Power Value (EPV)

Intrinsic value= EPV= Adjusted current earning x 1/R – Debt (interested bearing) + cash in excess of operating requirement

(R: cost of capital)

The important assumption of this method is that current earning level will last forever. It eliminates any potentially growing earning, however, according to the book, can be applied in both non-viable and viable industries, even growing industries.

Firstly, we have to figure out what type of earnings to use. In this case, it is the EBIT after tax. There are four adjustments needed to make:

– Rectify any accounting misrepresentations that are unconnected to normal operations. For instance, there is a year when company spent high “one-time” charges. We find average ratio of those charges bear to reported earnings before adjustment and have them averaged out

– Add back depreciation/amortization expenses and subtract maintenance capital expense (maintenance capex)

Maintenance capex can be calculated based on capital expenditure , which is reported in cash flow statement, and growth rate in sales. Capital expenditure consists of growth capex and maintenance capex.

We have:

Growth capex= (average, perhaps in 5 yrs) PPE/Total sales x Increase or decrease in sales (in term of dollar)

Maintenance capex = Reported capital expenditure – growth capex

– Take into account business circle: reduce reported earnings company is at its peak, and vice versa, raise earnings if company is in a trough; thus, we could smoother the earning trend.

– Any other adjustments

To estimate R, we base on Weighted Asset Cost of Capital, using after-tax cost of debt and cost of equity

- COMPARISON BETWEEN “VALUE OF ASSETS” AND “EPV”

Three scenarios happen when we calculate value of assets and EPV to measure intrinsic value of a specific company

– EPV < value of assets

– EPV = value of assets

– EPV > value of assets

In any cases, however, we will employ EPV as a benchmark for the intrinsic value. Depending on each case, EPV will be adjusted a bit.

When EPV is smaller than value of assets, it is possibly attributable to two reasons. Firstly, the industry is having excess overcapacity so the number of products consumed is less than of produced. Secondly, management of the company may not be effective in using assets to generate incomes.

When EPV is equal to value of assets, there is no doubt that we can use either one as intrinsic value. In this scenario, the industry is supposedly competitive and management is average.

Finally, EPV is larger than value of assets due to some reasons. The industry is not so competitive with barriers of entry somehow exist. Or, the company is possessing competitive advantages that help it employs assets efficiently and generates high profits. Another factor may be the high quality of management in the company. We will look into competitive advantage in the next chapter.

Whichever scenarios happen, we have to check back and forth between numerical results and information that supports those results. If a company is on the verge of bankruptcy but has EPV higher than value of assets, perhaps something is wrong. On the other hand, if we are sure about our techniques and EPV is still high, we must explore what factors that help the company gain superior returns and whether those factors are strong and sustainable.

When EPV > Value of Assets

When EPV is bigger than value of assets, the company is creating a special value called “Value of franchise” which explains why EPV is high.

Value of franchise

In order to create value of franchise, the company must possess strong and sustainable competitive advantages. Those advantages can be found in or out of the company’s control.

External favoured condition such as exclusive license provided by government can generate some advantages.

Internal factors are those that influence revenue and cost-the two components to calculate profit. First, from the revenue side, company’s products that are in high demand in the market will produce large revenue. High demand maybe a result of consumption purchasing habits as in Coke’s case. Revenue also endures if the cost of switching to alternative is expensive to customers. In some certain industries, customers are resist of any change in product used, for instance, office software. They do not want any change because it is expensive, complicated and risky. Thus, strong customer loyalty is an important factor that contributes to a success of a company. Second, in the cost side, the lower operating cost the higher profit company can earn. Hence, many companies want to save cost or use money efficiently. They can do it if they have special production techniques or products that competitors cannot match. They also may gain exclusive knowledge in making things efficiently by having technology or human-based skills. Third, cheap resources, especially labour and capital, can save significant costs. Finally, economies of scale: high fixed cost and minimal variable cost can make unit production costs reduce as long as sales increase.

However, an economy of scale does not work in some cases. If firms with same sizes of operations competing against each other, then they will have same economies of scale but the market at the moment does not need to absorb such a huge amount of product; thus, competition is tense between big firms in this case. Another scenario that diminishes economies of scale is when technology changes so fast and affects profitability of companies in the certain industries. Because the firms always need to spend money investing in business, cost advantage is short-lived. Furthermore, companies with economies of scale should use their power effectively by employing aggressive pricing power so that they could make full use of price opportunities.

Value of growth

Some firms with value of franchise possess another value called “Value of growth”, when growing in earning is bigger than incremental cost of capital to support the growth. To many value investor, this value of growth is uncertain because of 2 main reasons so they are not willing to pay for it. First, it is difficult to forecast specific growth rate in earning in the future. Second, that growth must be profitable. It is uncertain that for how long growth in earning can remain to be bigger than incremental cost. Thus, in case of suspiciousness, investors can buy stock at its full EPV and consider value of growth as margin of safety.

Thus, we have a formula:

PV of Cash flow/ EPV= Margin of safety

In which PV = Invested capital x (ROC-G)/(R-G)

EPV= Invested capital x ROC/R

ROC= Return on capital = ROE or ROIC

(ROIC=Operating earnings /operating asset (Debt +capital))

G= Growth in sales or in earning (or both)

Therefore, as long as ROC>R, increase in growth can generate additional value.

- CONSTRUCTING A PORTFOLIO

Diversification in constructing a portfolio is a way to reduce risks caused by volatility in stock prices. To value investor, however, they usually have more concentrated portfolios. According to them, risks do not come from volatility in stock prices but is the possibility of losing money. Volatility, in contrast, creates great chances for investors to buy discount stock. They also argue that correlation of securities in a diversified portfolio is hard to predict. Strength or weakness of correlation depends on many factors and that may be changed due to events or crises.

Value investors are confident in their concentrated portfolios partly because they tend to operate within the boundaries of their competences and invest in companies they can understand. Moreover, they are careful in choosing stock and sure that there is an adequate margin of safety. Large margin of safety is a good solution to limit risks. To build up their confidence, they look for credible confirmation of their opinion. Knowledgeable insiders and famous investors’ action are two sources to look at. In addition, value investors need to ask themselves critical questions: why not other investors in the market pile in to move up prices of bargain stock? Is there a value trap when the price is never going to increase?

To build a concentrated portfolio, investors can impose a limit that they will not buy a security if they are not willing to invest a meaningful amount in it (approximately 5% of portfolio). This position limit will help them to be cautious in selecting and evaluating a security since the money involved is large.

In case of excess money but there is no investment opportunity available, investors can spread it among existing investment or put it in index funds. Index funds, in general, will give investors greater return than hard cash.

♣ CLICK THIS TO STOP TRYING TO ACHIEVE YOUR GOALS BY YOURSELF AND BE COACHED TODAY HERE

♥ CLICK THIS TO DOWNLOAD THIS FREE PDF SUMMARY HERE

♦ CLICK THESE FOR THE FOLLOWING Book | Summaries | Course

YouTube |Spotify | Instagram | Facebook | Newsletter | Website